Every commitment to Lot 29 enters the same underwriting discipline, the same reporting cadence, and the same operator standard. Here is what that looks like in practice.

Lot 29 underwrites the way the institutions we work alongside underwrite. Our team has structured deals with Carlyle, Nuveen, and other major funds, and we apply that same rigor at every check size. Most private real estate sponsors run a single base case marketed as conservative. We don't operate that way.

The base case in our model already assumes a slower market than today's. Then we model construction cost overruns, interest rate shocks, hold-period extensions, exit cap rate expansion, and lease-up delays against that base. If the downside still produces a positive return, the deal earns capital. If it requires a perfect environment to clear, we pass.

Sale assumptions are anchored to closed comparable transactions, not list prices. Each deal package shows the exact closed sale we benchmarked against, with date, price per square foot, and unit-level detail. We don't quote ranges. We quote the trade.

Acquisition price has a defined walk-away. Above the target basis, the deal does not pencil at our return thresholds and we step aside. The deals we close are the ones where the math is honest at acquisition, not the ones where we hoped to renegotiate later.

Our build partner has executed at the highest finish tier in our submarkets. Contingencies, fixed-price subcontracts on the largest line items, and daily site oversight are budgeted from day one. Execution risk is mitigated structurally, not assumed away.

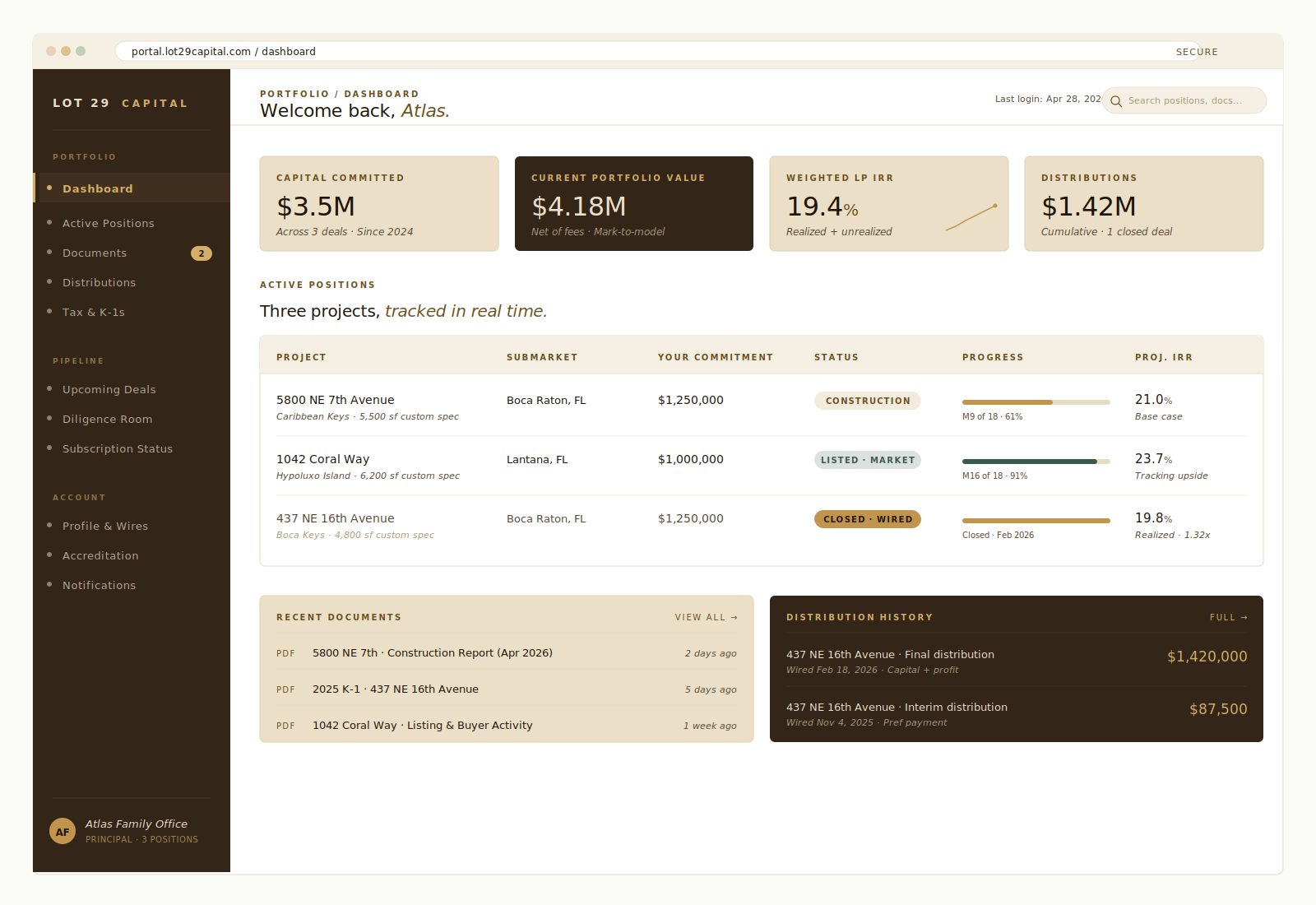

A dedicated portal for each capital partner. Construction progress, projected IRR, document access, distribution history, updated as projects advance.

Family offices and HNW partners receive the reporting cadence institutional LPs demand from billion-dollar funds. Quarterly capital statements, monthly construction draw photography, distribution history exported for tax prep, and a direct line to the principals on every position.

No IR-team gatekeeping. No quiet repositioning when a deal moves off plan. The same people underwriting the deals are the ones answering the calls.

Position-level statements showing capital deployed, current basis, projected timeline, and variance against original underwriting. Same format every quarter. Delivered to your inbox and posted to the portal on the first business day of each quarter.

Every construction draw documented with site photos, AIA pay applications, and lien waivers. You see what was built that month, what it cost, and what's on the schedule for the next month. No black boxes between contract and certificate of occupancy.

PPMs, subscription agreements, K-1s, capital call notices, and distribution notices for every deal, dated and downloadable. Audit trail of every document you've ever signed or received, organized deal-by-deal.

Questions go straight to the sponsor. Not through investor relations, not through a junior analyst. The same people underwriting the deals are the ones answering the calls. Founder cell on every commitment letter.

Every distribution you've received, when it was wired, against which deal, and what it represents, preferred return, return of capital, or profit share. Cumulative across positions and exportable for tax preparation.

Upcoming Lot 29 deals come to platform partners before they're shopped to broader capital. You see basis assumptions, comp work, and underwriting alongside us, with time to ask questions before commitment is structured.

Deal-by-deal participation through standalone vehicles. Sponsor commits 5–10% co-investment per deal, pari passu through the preferred return. Alignment is structural, not promised.

Each deal closes as its own standalone vehicle with a dedicated PPM, subscription documents, and offering structure reviewed by securities counsel. Capital partners participate deal-by-deal, there is no platform-level lock-up or blind pool commitment.

Minimum commitments sit in the six-figure range and are sized per deal. We share economics, waterfalls, and the underwriting model with prospective partners on request.

Lot 29 is led by Nick Ayala and team. Nick is a Series 65 licensed advisor with over 20 years across capital structuring and institutional real estate, who structures, underwrites, and oversees every deal across both tracks. Execution partners are contracted per track and per asset.

Private real estate carries materially different tax treatment than public market investments. Most of the value sits in three places.

Builds and multifamily acquisitions generate depreciation that flows to LPs via K-1. On stabilized multifamily, cost segregation studies often accelerate this meaningfully, offsetting distributions and creating paper losses in early years.

Builds held over 12 months and multifamily exits qualify for long-term capital gains, materially below ordinary income rates for most allocators.

When a multifamily deal lands in a qualifying location, capital gains deferral becomes available. Builds are held for sale and do not qualify; multifamily often does.

Tax treatment varies by investor and deal structure. We coordinate with your CPA on every commitment.

Every deal is structured to manage these. We surface them now so the conversation later is about fit, not surprises.

Capital is committed for the life of the deal. Builds run roughly 18 to 24 months; multifamily holds 3 to 5 years. Plan accordingly.

Schedule and budget variance is part of building. We carry contingencies, fixed-price subcontracts on major scope, and daily site oversight to keep it in check.

Build exits move with the housing market. Multifamily exits move with cap rates and rent growth. We stress-test against meaningful softening on both.

Multifamily assets carry leasing, occupancy, expense, and capex variability through the hold. Underwritten with realistic vacancy and reserves.

Each deal is its own vehicle. Diversification comes from participating across multiple deals over time.

Deals use debt, which amplifies both upside and downside. Conservative LTC/LTV targets and rate stress-testing are part of every underwriting.

The fastest way to understand whether Lot 29 fits your portfolio is a single call. We walk through the active deal, the underwriting, and the structure. No deck-of-the-week, no follow-up cycle.